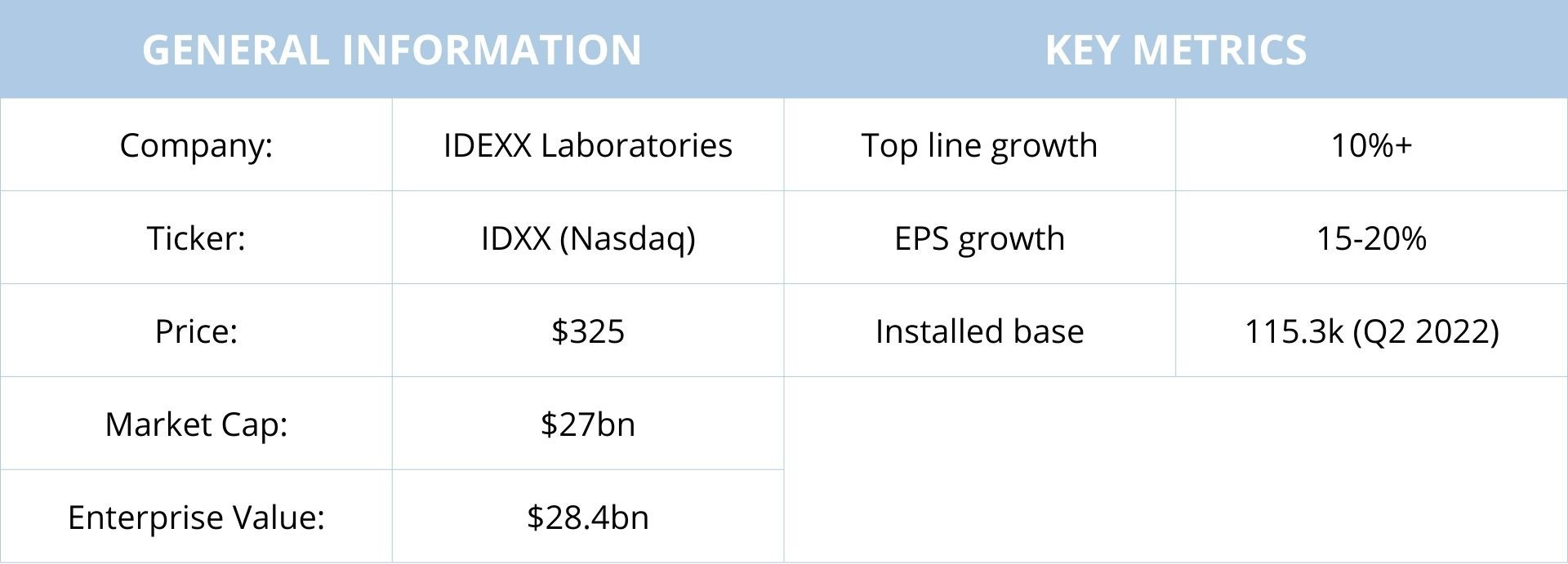

IDEXX Laboratories, Inc.

Deep dive analysis

SUMMARY

IDEXX is a global leader in diagnostic services and solutions for the companion animal veterinary, livestock, poultry and dairy, and water testing markets worldwide. Each business is innovation-driven, with expertise centered on diagnostics and increasing integration with information management. As a result, these businesses have a growing recurring revenue base that generates predictable, durable, high incremental gross margins. These dynamics support strong operating profit gains and excellent returns on invested capital.

CONTENT

BUSINESS OVERVIEW

INDUSTRY

MOAT

COMPETITION

MANAGEMENT

FINANCE

UNIT ECONOMICS

CAPITAL ALLOCATION

VALUATION

WHAT COULD GO WRONG

1. BUSINESS OVERVIEW

IDEXX develops, manufactures, and distributes products and provides services primarily for the companion animal veterinary, livestock and poultry, dairy, and water testing industries. The company also offers human medical point-of-care and laboratory diagnostics. The company operates through the following business segments:

Companion Animal Group (90% of 2021 revenue) - IDEXX's primary business is providing companion animal diagnostic products, services, and software solutions that deliver clinical insights to veterinarians. For 2021, recurring diagnostic revenue accounted for approximately 80% of consolidated revenue.

The core CAG business has long-term secular growth characteristics, such as the growth in the global pet population, the deepening bond between pets and their owners, and veterinary customers' intent to provide a high medical standard of pet care.

Water quality products (5% of 2021 revenue) - provide innovative testing solutions for detecting and quantifying various microbiological parameters in water. The water tests are used by government laboratories, water utilities, and private certified laboratories to test drinking water in compliance with regulatory standards.

Livestock, Poultry, and Dairy (4% of 2021 revenue) - provide diagnostic tests, services, and related instrumentation that are used to manage the health status of livestock and poultry and to ensure the quality and safety of milk and food. Government and private laboratories purchase livestock and poultry diagnostic products. In addition, dairy producers and processors use dairy products worldwide to detect antibiotic drug residue in milk.

Other operating segments (around 1% of 2021 revenue) - combine and presents human medical diagnostic products and services business (OPTI Medical) with out-licensing arrangements.

R&D expenses are around 5.0-5.5% of our consolidated revenue.

As of 31 December 2021, IDEXX had approximately 10,350 regular full-time and part-time employees. In 2021, the voluntary employee turnover rate was around 12%. Voluntary turnover among managerial and professional staff was about 6%. The most recent global employee survey indicated an 82% engagement level.

2. INDUSTRY

The typical U.S. annual pet population growth has been in the 1% to 1.5% range. As a result, the total pet population is around 177 million at the end of 2021.

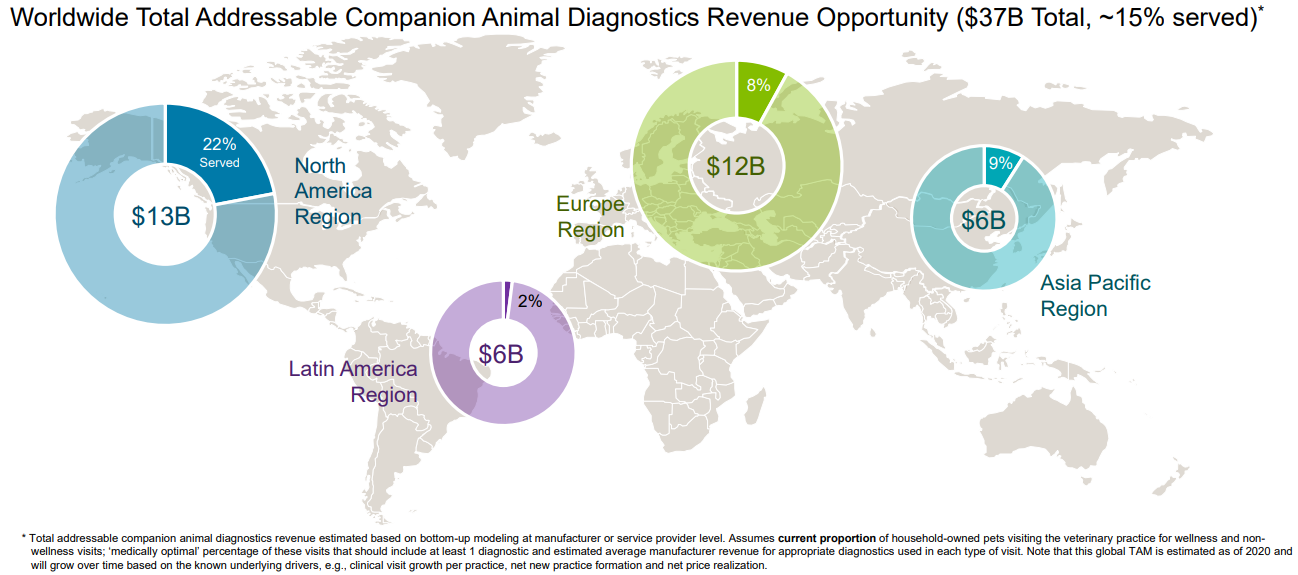

According to the Company, the worldwide total addressable CAG revenue opportunity is around $37bn. Therefore, approximately 15% of the potential $37bn TAM is served today.

In addition, the average annual increase in veterinary care for the past 15 years has been +5% to +10%.

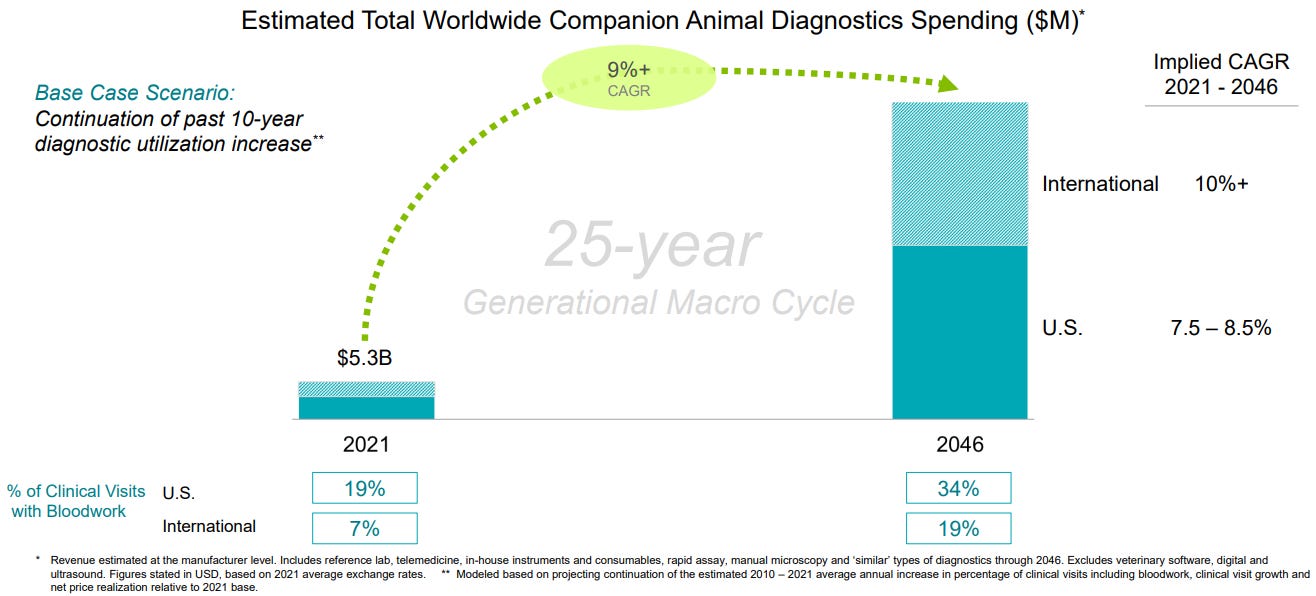

In 2021, IDEXX estimated the global sector for companion animal diagnostic revenue at the manufacturer level at about $5.3bn, with blood work at 19% of clinical visits in the U.S. and a much lower estimated 7% in international regions.

For the U.S., if we project a continuation of the increase in diagnostic utilization observed over the past 10 years to continue over the next 25, this would imply compound average annual Diagnostics segment revenue growth of 7.5% to 8.5%, and the U.S. would reach about 33% of clinical visits, including blood work in 2045.

IDEXX views this as reasonable as an outcome in the year 2046 for the U.S. since this would mean we would be reaching approximately what we see today in the top decile of U.S. practices. For international, if we assume the average blood work utilization reaches today's U.S. level of diagnostic utilization in 25 years, this implies compound average annual international Diagnostics revenue growth of 10%+.

3. MOAT

The breadth of the total diagnostic solution and the seamless software integration of IDEXX's offering provides a differentiated competitive advantage.

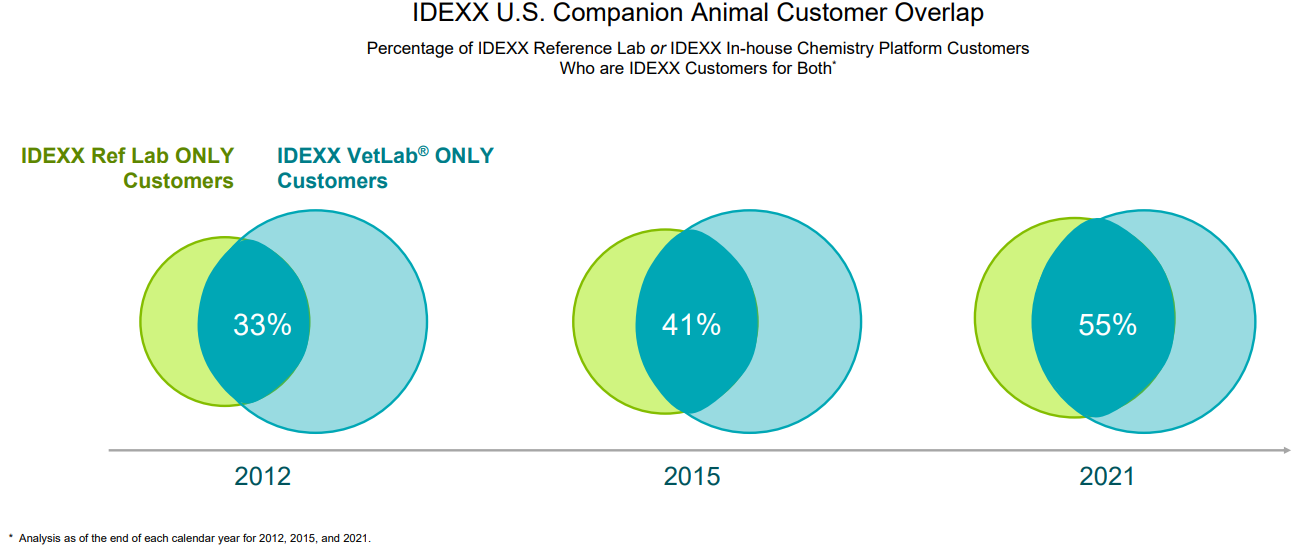

As a result, more than half (55%) of U.S. customers partner with IDEXX for all their diagnostics needs.

If you double-click on that 55%, more than 50% of those customers use practice information management systems (PIMS).

The synergy between IDEXX diagnostics and software is quite powerful. When customers are all-in with IDEXX, whether large or small, their recurring diagnostic revenue is up more when they use the Cornerstone practice management software than when they use non-IDEXX PIMS. This intuitively makes sense as all testing activities are captured automatically, and workflow seamlessly integrates.

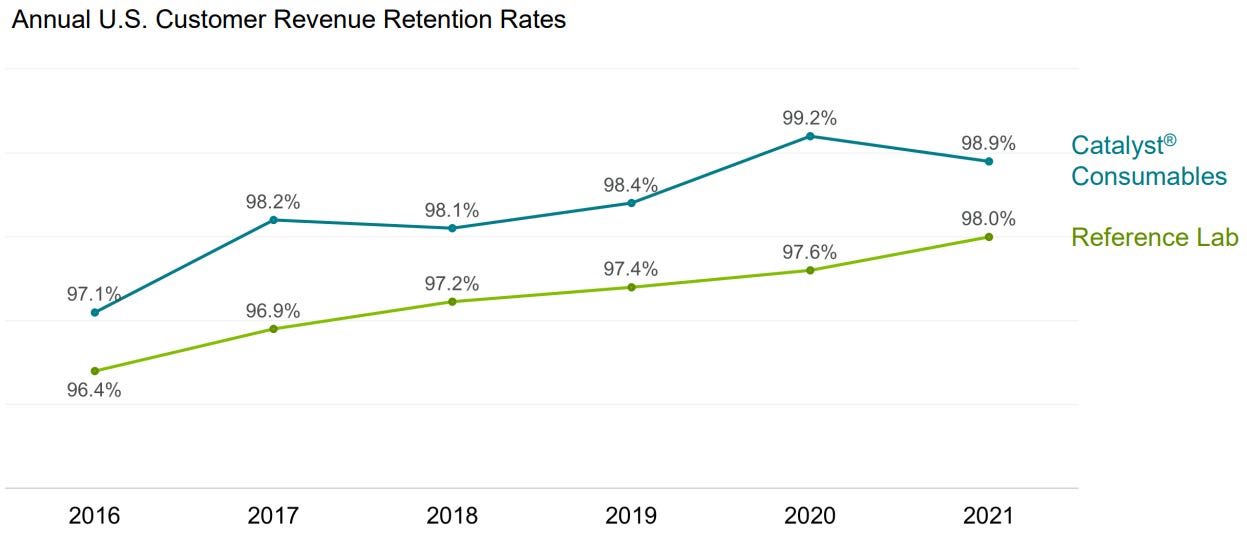

In 2021, U.S. consumable revenue retention reached nearly 99% and lab revenue retention 98%. In addition, the rapid assay front has retention levels for its core vector-borne disease tests around 97%.

4. COMPETITION

In companion animal diagnostic offerings, the major competitors in most geographic locations in North America are Antech Diagnostics, Zoetis (including its wholly-owned subsidiary Abaxis), Heska Corporation, and Samsung Electronics. IDEXX also competes in specific international geographies with Zoetis, Fujifilm Holdings Corporation, Samsung Electronics, Arkray, Heska, Mindray, and BioNote for pets.

In water, livestock, poultry, and dairy testing products, competitors include smaller companies and multibillion-dollar companies with small livestock and poultry diagnostics and water testing solution franchises.

In veterinary software, services and diagnostic imaging systems, the largest competitor in North America and the U.K. is Covetrus, which offers several systems and leverages its animal health distribution business in sales and service. IDEXX also competes with numerous focused smaller companies throughout the geographies offering veterinary software, including those offering cloud-based solutions. Competitors in the diagnostic imaging systems include Sound-Eklin, Antech Diagnostics, Fujifilm, and Heska.

Human medical diagnostic products compete primarily with large human medical diagnostics companies such as Radiometer, Siemens Medical Solutions Diagnostics, Instrumentation Laboratory Company, Abbott Diagnostics, a division of Abbott Laboratories and Roche Diagnostics Corporation. They also compete with many companies worldwide that produce human COVID-19 testing.

5. MANAGEMENT

IDEXX has long-tenured management. In 2019 CEO Jon Ayers stepped down after 17 years with the company due to a bicycle accident. Jay Mazelsky has been President and Chief Executive Officer of IDEXX since October 2019 (internally promoted). He joined the Company in August 2012. Brian McKeon joined in July 2003 and became CFO in January 2014.

6. FINANCE

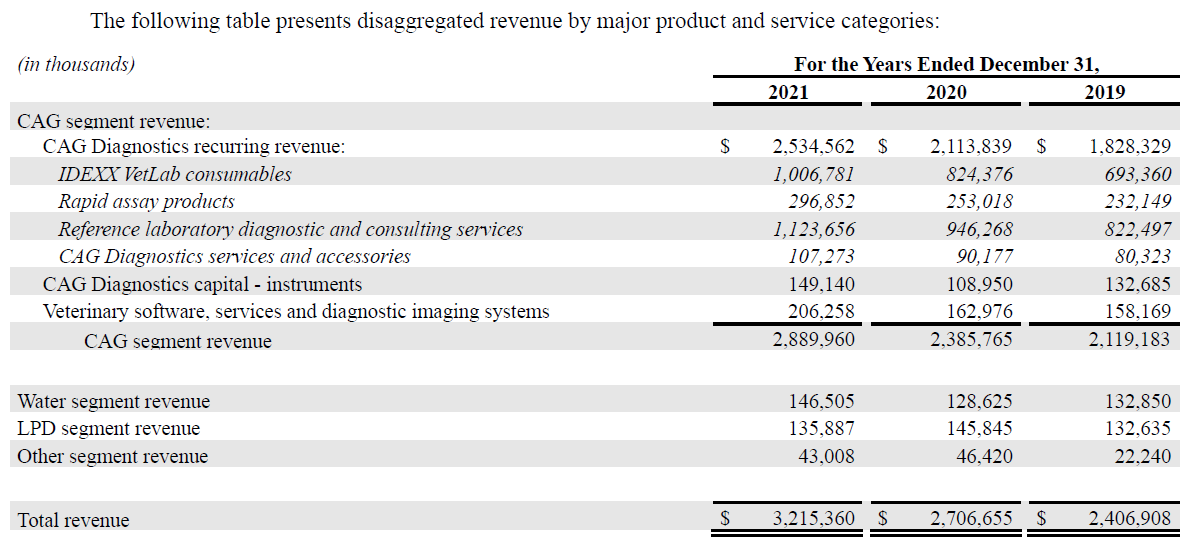

Top line development 2019-2021:

Diagnostics instruments development:

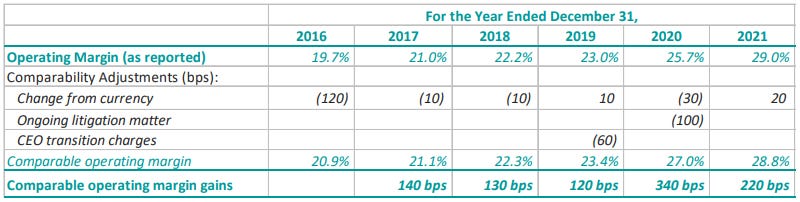

Operating margin development 2016-2021:

7. UNIT ECONOMICS

A key metric IDEXX focus on is the incremental gross margin they earn as they increase growth in core areas.

For example, the incremental gross margins that flow from in-clinic diagnostics from adding services to scale reference laboratory base and expanding cloud-enabled software and digital imaging services are at 60% or higher.

In addition, IDEXX has a consistent and very high return on invested capital.

8. CAPITAL ALLOCATION

CAPEX – around 4-5% of revenues.

Dividend - never declared or paid any cash dividends on the common stock.

SBB – ongoing program. Due to the COVID-19 pandemic and its impacts during 2020, IDEXX suspended SBB activity in the first quarter of 2020. However, they resumed share repurchases during the first quarter of 2021. From the inception of the SBB program in August 1999 to 31 December 2021, they have repurchased 68.0m shares for $5.0bn. In 2021, they purchased 1.3m shares for an aggregate cost of $755.5m, compared to purchases of 0.7m shares for an aggregate price of $179.6m during 2020. Since the inception of the SBB program, IDEXX repurchased over 40% of the company's outstanding shares for an average price of $32 per share (split-adjusted).

M&A - IDEXX acquires small reference laboratories or radiology practices from time to time.

Debt - low leverage levels and a well-phased tenor to the current debt structure.

9. VALUATION

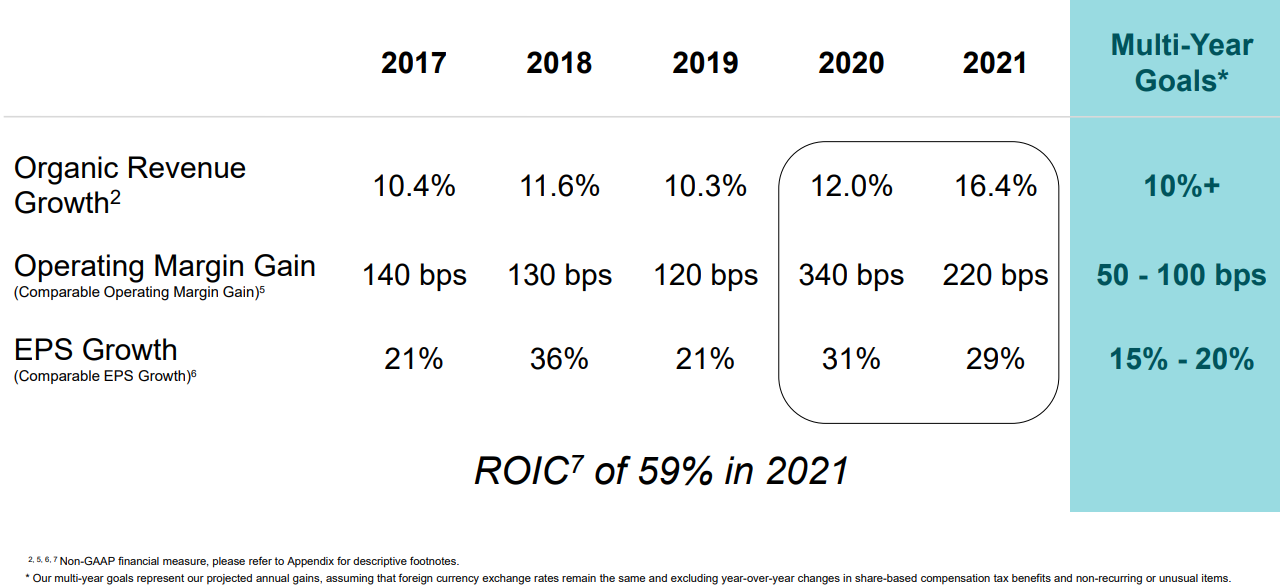

IDEXX has achieved an average of 12% organic revenue growth over the past 5 years, 28% average comparable EPS growth, and 59% return on invested capital.

IDEXX plans to continue 10% plus organic growth with high returns for investors.

My assumptions: (i) Top line growth 9% (average) until 2032; (ii) Cash flow from operations margin 25%; (iii) Capex 4% of sales; (iv) WACC 8%; and (v) Terminal multiple 16x. Based on the inputs, my fair value is $18.6bn market cap or $221 per share.

10. WHAT COULD GO WRONG

When someone analyses the risks IDEXX faces, it should be aware that the Company manages the global business and the related risks.

The first risk is related to the macroeconomic environment. Given its sensitivity to improving or deteriorating macroeconomic conditions is relevant.

Further, failure to anticipate changes in the market environment (new customer requirements and competition). It should be clear that IDEXX operates in a competitive market. IDEXX's business lines are highly attractive. However, they are also highly attractive to competitors.

The US dollar's fluctuating performances against the other currencies pose both upside and downside risks.

New COVID-19 virus variants could extend the pandemic and once again disrupt economic activities.

Over-estimated the current industry trend and over-earning the existing customer base.

There are many other risks that IDEXX face and some of which I am not even aware.

Disclaimer: This is not investment advice. Always do your own research. I do not assume any liability or guarantee for the information's accuracy and completeness. I am not a registered investment adviser and may or may not hold the securities discussed in this post/blog.